How Can You Improve Your Credit Score

Credit scores are an important part of almost any major financial decision. Whether you are looking to purchase a car, take out a mortgage, or simply apply for a new credit card, a credit score can make or break how good a deal you get.

Unfortunately, one out of ten Americans have either never checked or don't know their credit score. Even consumers who understand the importance of this information don't check it every year.

Not knowing if they have poor credit leads many borrowers to accept bad loans and deal with interest rates that they, frankly, can't afford.

And with the pandemic coming to a close and more and more people making significant financial decisions, every consumer must understand how to improve their score and increase their chances at receiving a good loan.

With that in mind, let's take a look at how credit scores can be used alongside alternative credit tools, like Connect, to demonstrate your creditworthiness and receive the loan you need today!

What is a Credit Score?

Understanding the significance of your credit score in the loan approval process can be confusing. That's why we will pinpoint the most important facts you need to know about the scoring process. Let's take a look!

Even though versions of "credit scores" have been used throughout history, it wasn't until 1980 when lenders truly began seeing the value in using a scoring method to measure a customer's creditworthiness.

In 1989, the first credit scoring model, the FICO score – coined after its creator, the Fair Isaac Corporation – was built to help lenders get a more accurate understanding of traditional credit data.

This scoring system was revolutionary because it was the first method that accurately gauged a potential borrower's risk based on their credit history.

Much later, in 2006, the VantageScore model -- developed by the major consumer credit reporting agencies, Experian, Equifax, and Transunion— was developed in the hopes that it would provide competition while allowing more consumers access to credit.

Although both methods are still widely used, FICO scores are easily the most important model, with 90 percent of the consumer credit reporting companies using it over the VantageScore.

Because of the drastic difference in usage, we will focus more heavily on FICO scores throughout this article. If you want to improve your VantageScore specifically, click here.

Note that although traditional credit information is commonly used, alternative credit is quickly becoming an essential factor in determining someone's actual creditworthiness.

How are Credit Scores Calculated?

The makeup of credit scores can often be a confusing subject. In fact, around 40 percent of Americans have no idea how their score is calculated.

So, if you are unsure, or at least don't completely understand the method behind the madness, let's go over the basics.

Essentially, all your financial data, such as your address, employment history, detailed bank account information, etc., is sent to consumer credit reporting agencies and compiled into a credit report.

It's then inputted into a scoring model, which determines where you fall on a scale from 300 to 850. Although you always should aim to have a perfect 850, having anything over 690+ is great!

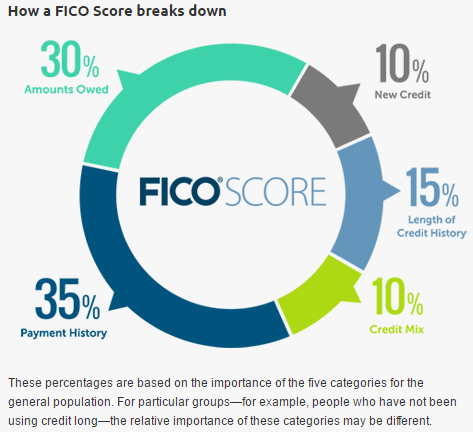

You may be asking, "what factors allow them to come up with this magical number?". While the full answer is not simple, it, thankfully, can be broken down into five critical categories:

- Payment History: The most crucial element of your credit score, this component is calculated based on how often you pay your bills on time. This should be the number one factor you consider.

- Amounts Owed: Fancy terms like credit utilization rate are often tossed around with this element, but all you really need to know is that if you make consistent progress reducing your debts, then you are in the clear!

- Length of Credit History: The longer you've been using credit to make purchases, the easier it is for consumer credit bureaus to determine your creditworthiness.

- New Credit: Opening new forms of credit can be good, but it may result in a decrease in your score if done too often. This is caused by lenders conducting hard inquiries.

- Credit Mix: Diversifying credit is usually good for your report and can show how responsible a borrower can be. Unfortunately, if you take on too many accounts in a short time, you may end up damaging your score.

Note that credit scores are not always the same, and each consumer reporting agency calculates a higher or lower score based on the above factors.

How Do I Get My Credit Report/Score?

Let's tackle credit reports first. The easiest way to pull your credit report is to go to annualcreditreport.com and click the "Request your free credit report" button. It's as easy as that!

In fact, now is one of the best times to do this because the Federal Trade Commission (FTC) has temporarily allowed all Americans to receive a free weekly credit report due to the pandemic.

Normally, you would only be able to pull one report from Experian, Equifax, and Transunion each year.

Take this opportunity to check it weekly, or monthly, and see how your financial decisions impact your report to determine what changes you might need to make in the future.

Similar to credit reports, there are also free ways to get your credit score. Be careful though, because, unlike credit reports which are required by law to be made available to you, scores may require you to provide extra information and/or pay money.

A good solution is to use Credit Karma (mainly because they don't require credit card information from you), BUT you need to do the research and find the best method that fits you.

Note that although people claim that requesting a credit score will damage your credit report, they are entirely wrong! Unlike the hard inquiry mentioned earlier, if a consumer requests their own credit score, it will be considered a soft inquiry and have zero effect on your report.

I Have No Credit Score?!

You might have asked for your credit score and came up with nothing. Do not panic. This is most likely due to a thin credit file.

A thin credit file means you don't have enough data to generate a credit score. Although this may seem odd, approximately 64 million Americans have this issue. But there are ways to fatten up your credit report.

How can I improve my score?

Now that you have a basic understanding of the credit scoring process, we can start addressing the big question, "How can I improve it?" This question is asked by over a quarter of low-income Americans who don't know how to raise their score.

Thankfully there are tons of methods to accomplish this! Let's go over the top ten ways to improve your traditional credit score:

- Get a Handle on Bill Payments: Paying your bills on time is one of the simplest and best ways to improve your score. The less often you are late on payments, the more likely lenders will see you as a responsible consumer.

- Become an Authorized User: If you have a family member who has demonstrated their ability to pay bills on time – and their credit score reflects that – then you may want to consider making yourself an authorized user. Their data will supplement yours and may give you a significant boost.

- Dispute Credit Reports: Although financial institutions are usually careful with data, you should never fully trust they will get everything right. Twenty percent of Americans have at least one error on their report. That's why you must make use of your free credit reports!

- Protect Your Personal Information: Someone's identity is stolen every second. Being a victim of identity theft can damage your credit score immensely, so be sure you have proper measures in place to protect your data.

- Avoid Credit Repair Scams: There are quite a few of them out there that promise they can make negative information on your credit report magically disappear. Don't trust them! No company is legally allowed to delete accurate information from your file.

- Pay Off Credit Card Balances: Using a credit card can be a great way to improve your credit score, especially if you have a card designed for it. But it's only truly useful if you are paying the balances off on time. Look into automatic balance payment options to make this easier.

- Limit Your Requests for Hard Inquiries: The more credit card, mortgage, or auto loan applications you have opened at one time, the more likely your score will decline. Space out your major transactions, and you can avoid taking a hit.

- Keep Old Accounts Open: The longer you have an account open, the more beneficial it is for your score. Note that closing an account will not result in it being deleted from the credit report, but it can knock a few points off.

- Credit Monitoring Services: There are tons of services that can help you keep track of your credit, so you aren't left in the dark. The best part is many of them are free and can also protect you from identity theft. Check out some options here.

- Diversify Your Credit Portfolio: Having a wide range of loans to pay can help improve your score. Although it only contributes 10 percent to the entire FICO score, taking advantage of this can give you the small boost you need.

Be aware that credit reports are updated every 45 days, so it is not likely that your score will instantly jump up. It's important to be consistent and, more importantly, patient.

Alternative Credit Can Help!

Whether you have a good or bad score, everyone should be using alternative credit as an easy way to help show your creditworthiness to lenders.

Unlike traditional credit, an alternative score is built from data based on everyday expenses such as phone/utility bills and paying subscription services on time. The data is then compiled and transformed into a number between 100 to 850.

Many consumers question the validity of using anything other than a traditional score, but according to the Equal Credit Opportunity Act (ECOA), if you provide a lender with proof of nontraditional payment history – meaning your alternative credit score –, they need to take it into consideration.

Legally, a business can't turn you away by saying they only accept traditional credit reports. And most wouldn't want to.

Due to younger generations choosing more unconventional banking options than ever before, it should come as no surprise that traditional reports often struggle to pull enough data to create a comprehensive credit score.

A recent survey found that 68 percent of Americans prefer to use their debit card over their credit card when making everyday purchases. This means a lot less data in traditional credit reports.

To get your alternative credit score check out Connect. We are a 100% free service which will not only give you your alternative credit score but will help you manage and organize your bills and accounts.

We understand how difficult it can be to manage your score, especially after the pandemic, and that’s why we are allowing anyone to use our service as many times as they want.

At the end of the day, banking decisions are never easy and you can feel stuck in the approval process forever. But dealing with your bad credit can make a world of difference. So, before you go to another lender, make use of all the tools available to you and ensure that the next offer you get is one you can accept!