Alternative Credit Bureaus

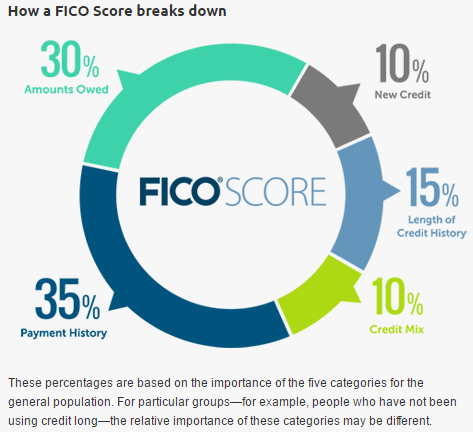

FICO has had a huge impact on the everyday lives of millions of Americans. Would you be able to get the mortgage to afford the new house? Will you be approved for that credit card? All of this is directly influenced by the consumer’s FICO score. It is important to understand what does a FICO score entail and how it is scored. The below representation is for an average customer and this may change for customers with different lengths of credit history.

FICO

FICO basically takes into account the credit report supplied by credit bureaus. Experian, Equifax

Credit Invisibles

The solution for credit invisible is leveraging alternative data to model and predict the behavior of the user. FICO in collaboration with Equifax and LexisNexis Risk Solutions has launched FICO Score XD and TransUnion has launched CreditVision Link to enhance its coverage of the American adult population. “ In testing, FICO XD allowed more than half of credit card applicants who were previously unscorable to receive a score”, said Jim Wehmann, executive vice president for scores at FICO. TransUnion reported that CreditVision allowed it to score 95% of Americans and resulted in 24% more loan approvals in a pilot with an auto lender. So what is the new data which has resulted in such a sharp jump in “

Alternative Bureaus

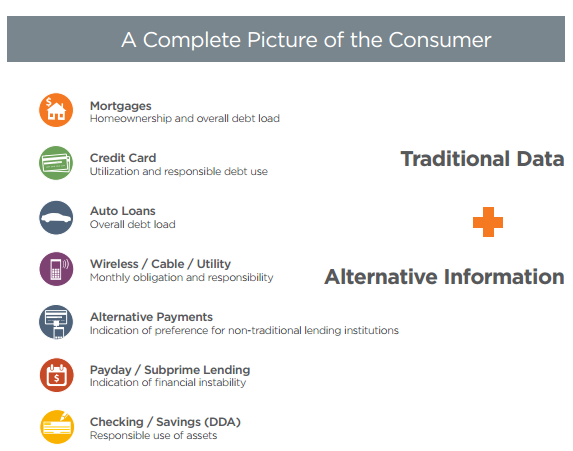

Going even further, PRBC.com offers a great alternative to FICO’s XD product. PRBC uses monthly-bills payment history, income data, cash flow data, account receivables, account payables, payroll, and outside investments to provide a complete picture of a financial profile. This allows PRBC to evaluate all Americans that pay regular bills. Unlike FICO, a consumer can self-register on PRBC.com and report their own scores. Companies like Envestnet-Yodlee and ID Analytics have launched alternative data solutions as well. Envestnet® | Yodlee® Risk Insight claims to incorporate data elements that are not available through the credit bureaus. ID Analytics has Credit Optics®, an FCRA compliant credit score which uses a repository of consumer behavior data sourced from a wide range of industries. The cross analysis of the alternate data with the traditionally available information helps solution providers present unique insights to lenders and others users.  Mortgages, Credit Card utilization, and auto loans represent the traditional data. Telecom, cable and utility bills and payments represent the new paradigm for credit analysis and scoring. Checking and

Mortgages, Credit Card utilization, and auto loans represent the traditional data. Telecom, cable and utility bills and payments represent the new paradigm for credit analysis and scoring. Checking and

Alternative alternative-data

Start-ups have already jumped on this bandwagon a decade ago when they started utilizing parameters like time of application, use of upper case in the online forms and amount sought as a loan. Lenddo, a

Limitations of alternative data

The new credit rating system might be a boon for some, but not for all. Credit challenged individual dependent on short-term loans or families behind on their utility dues because of peak bills in winters will be heavily penalized. Currently, the utilities only reported the serious delinquents to the credit bureaus, but this move will certainly push down the credit ratings of many Americans. Also, there is fear among consumer advocates that lenders can selectively target this data to exclude traditionally credit challenged minorities. Another lament is on the accuracy of the data provided by

The new normal

Alternative data is going to be the new normal is a foregone conclusion. Easier accessibility to large troves of consumer information and our digital imprint