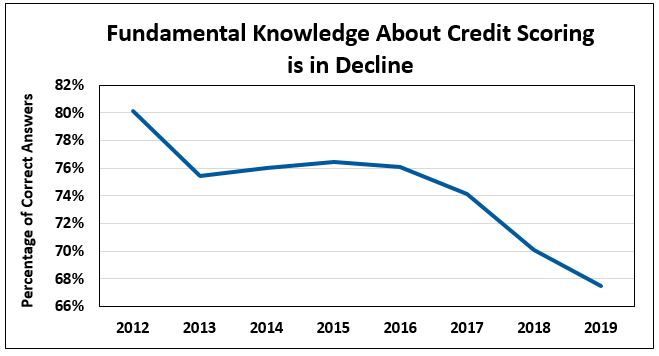

Consumer knowledge about credit scores reaches 8-year low

In 2010, roughly 50 percent of Americans checked their credit reports. Fast-forward to 2019 and, according to the Consumer Federation of America, the number of consumers checking their credit scores on a routine basis has increased. However, their fundamental knowledge of credit scores has decreased.

Consumers don’t fully understand their credit scores

Credit scores are widely available to consumers through their credit card companies, banks, and numerous other resources. While more Americans know to check their scores in 2019, basic knowledge about them has declined – the Consumer Federation of America says consumer knowledge about credit scores is at its lowest in eight years. In 2012, statistics showed 78% of people knew they had more than one credit score. In 2019, this number has dipped to 62%.

{kind=link}

Furthermore, CNBC reported in 2018 most Americans don’t understand that their credit score impacts their financial health, indicating just one-fifth of Americans understood how a low score affects interest rate charges.

Why it’s important to understand credit scores

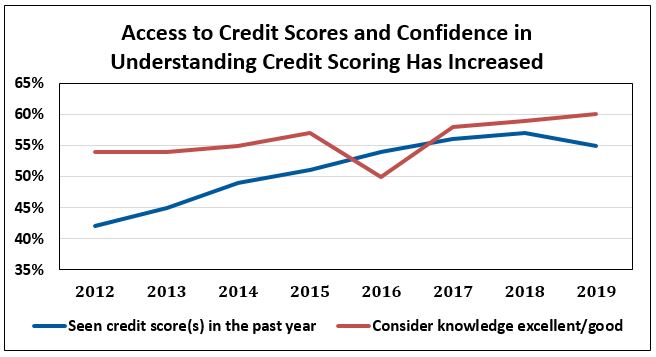

Many people also don’t understand how a bad score can have a direct impact on their lives – yet statistics success their confidence levels about understanding credit scores have increased. This could provide a false sense of security. It’s important to understand your credit score and how it works, because a low score can negatively impact you in many ways:

{kind=link}

- You can be denied access to the credit you need.

- Interest rates on loans will be higher if you are approved.

- Utility and cellphone companies may charge you higher deposits.

- You might have difficulty finding a job.

- Landlords may not rent you an apartment.

- Insurance companies will charge you higher premiums.

As you can see, there are many negative consequences of having a low credit score. It’s in your best interest to check your score at least once a year and, if it’s on the low side, work to raise it.

What you should know about alternative credit scores

Most people are familiar with the traditional credit score models, but did you know you can also get an alternative credit score by simply paying the bills you’re already paying? Connect’s model takes into account your payment history of bills such as your utilities, phone, internet, and even subscriptions. The credit score calculated by Connect works a lot like traditional credit scores, but we take a different approach. Instead of using the small datasets used by other scoring agencies, we take a holistic view of how you pay all of your monthly bills.

If you’ve found yourself in a situation where you have a low credit score, Connect can help. Our alternative scoring method can enable you to build your credit through a commitment to pay your monthly bills on time. To find out more about our services and how we can help you to re-establish your good credit standing, contact us today.